Bridging the data gap one consensual data transfer at a time

Neeti Bhatt

Senior Research Fellow, D91 Labs

Monami Dasgupta

Head of Research, D91 Labs

9 Aug 2021 — D91 LABS — FREE YOUR DATA

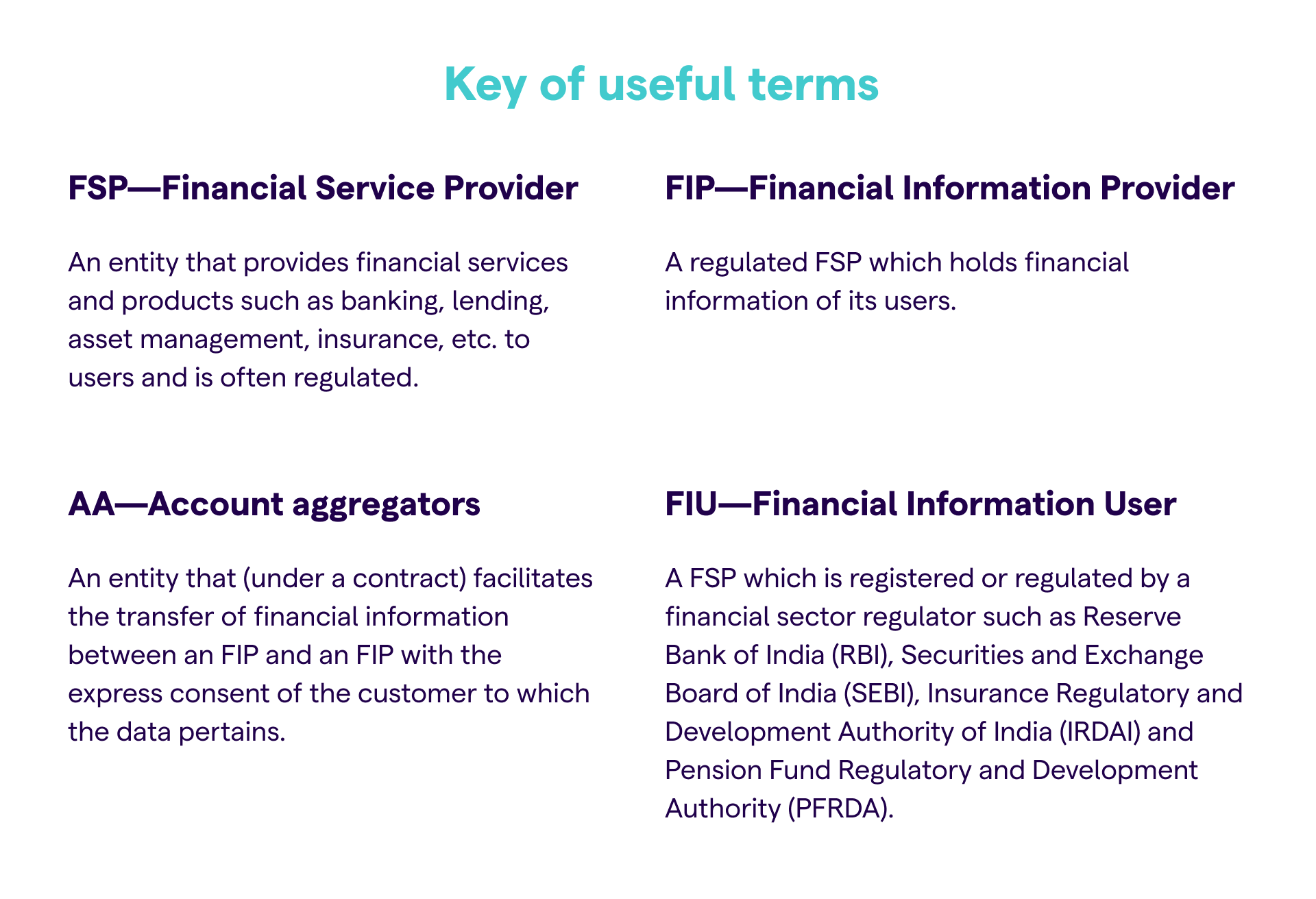

ACCOUNT AGGREGATOR

This article was co-authored by Neeti Bhatt and Monami Dasgupta of D91 Labs.

Let us weave you a story of Jigneshbhai, an upstanding member of a small village in Gujarat in the late 1960s.

Jigneshbhai spent most evenings with a small cohort of businessmen in his village discussing the ‘state of nations’ over chai, but his day job was as a small-time money lender to these businessmen. From his strategically located shop in the village square, Jigneshbhai could observe and map the schedule of all his ‘dendaars’ (borrowers). A slight change in route or an unscheduled absence sent him into a spiral of worry over the repayment of his funds.

Jigneshbhai and moneylenders like him are experts at judging the two crucial components of creditworthiness—the ability and willingness to repay borrowed funds. Their intimate knowledge of the lives of their borrowers makes it possible for them to ascertain with accuracy their net worth and trustworthiness. Of course, village gossip plays a massive role in providing this intel.

This approach, while effective in a small market, is not scalable. In order for institutional FSPs to do what Jigneshbhai does, they need a digital equivalent of his information aggregating skills.

For a user that has availed of a financial product as simple as a savings or salary bank account, a copy of their bank account statement can be a telling representation of their financial assets, liabilities, cash inflows and outflows. This is because bank statements show how much money they earn, where they spend their money, how many fixed obligations such as bills/ rent/ EMIs against loans do they have? As a user expands their pool of financial products and services, the financial information available in their name with the FSPs they sign up with also becomes more robust. This data is a critical component in determining their net worth and their trustworthiness and also their overall financial health. All of which make the user eligible for more financial products and services!

Therefore, it logically follows that each FSP that a user signs up with has financial information about this user. So, where does the FSP obtain this information in the first place? At present, any FSP that wants access to this information must request the user to provide that information (more often than not from other FSPs such as their banks). This manner of accessing the financial information can be time consuming and cumbersome, especially if done manually which is still prevalent in large parts of the country.

So is there a way to make this easier and more efficient?#

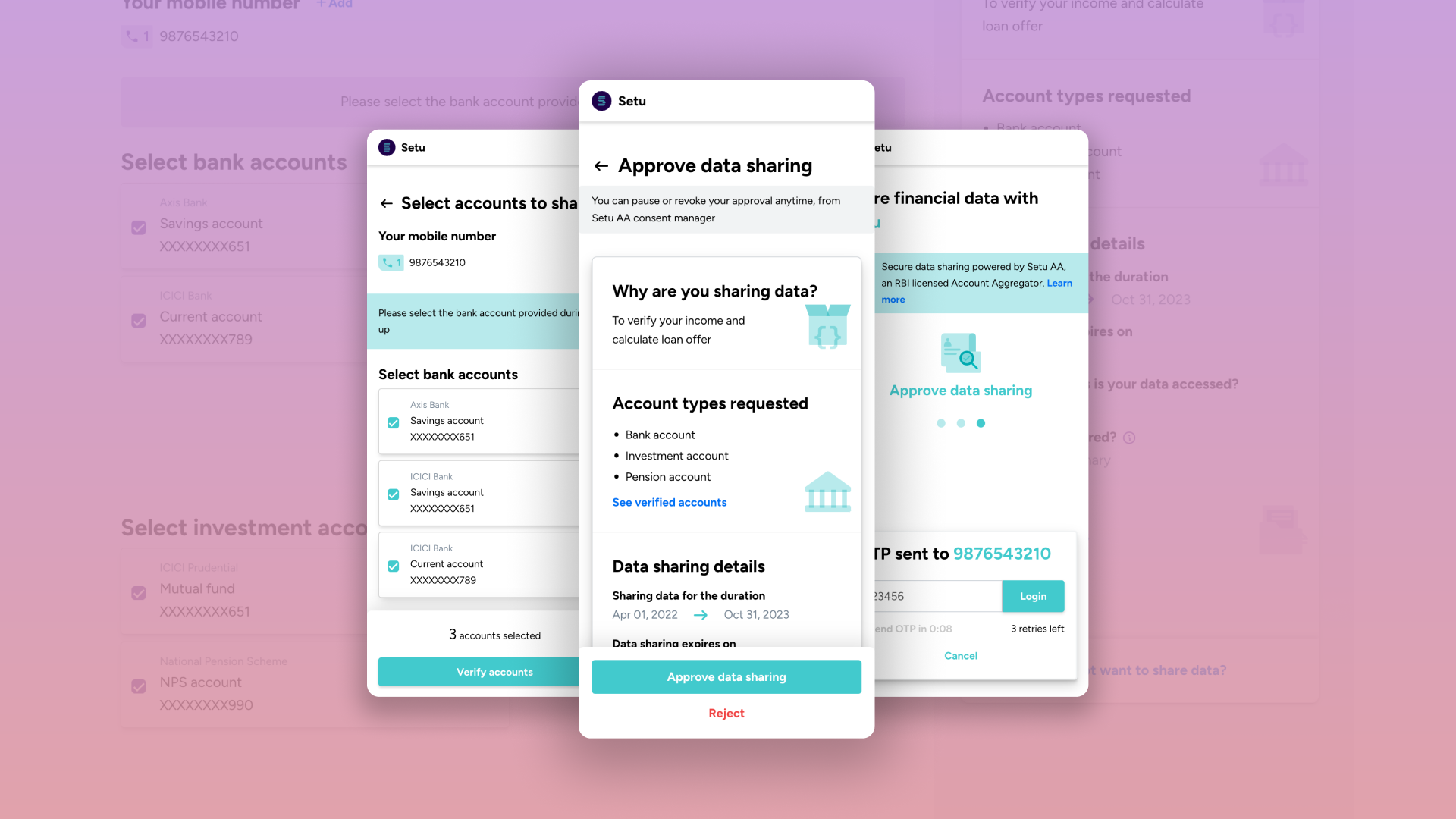

The account aggregator framework promises to do just that and what’s more—it is with the user’s explicit consent!

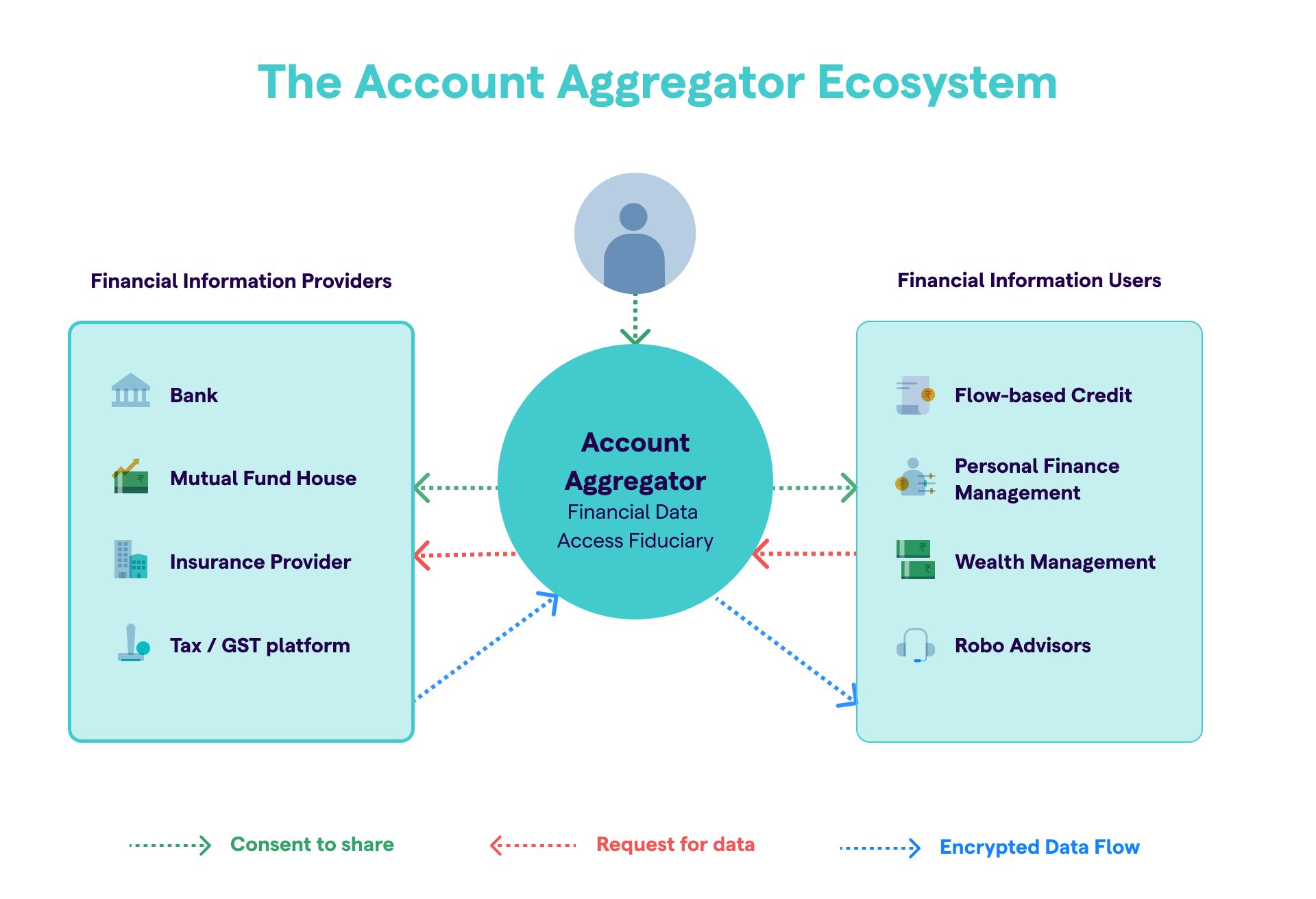

Simply put, an AA is a ‘data bridge’ between various actors within the financial products and services ecosystem.

An FIU that requires information about a user can directly approach a FIP (of the same user) through the AA framework and with the consent of the user can pull the necessary financial information of the user without multiple actions on part of the user. This consent of the user is the cornerstone of the AA infrastructure and is what makes a data pull through an AA framework between an FIP and FIU of the user transparent and therefore attractive. The consent and approval mechanics is the only substantial action on part of the user under the AA framework and this makes the user experience of accessing additional financial products and services much simpler. Consequently, the user holds complete autonomy over their data and the AA remains data blind through the swift and secure transfer of this information between the FIP and FIU.

Today, if Jigneshbhai was a registered lender and were to contract with an AA, he could request data on a borrower (including KYC, bank statements, cash flows statements, insurance policies, investments, tax returns etc.) from other FSPs that were willing to provide this information directly. With a click of a few buttons and the consent of the borrower, Jigneshbhai could access this information, make more precise lending decisions and avoid having to keep such a watchful eye on the everyday lives of so many.

Can AAs do more than reduce bureaucratic paperwork?#

It’s clear that AAs can make the process of financial information transfer much simpler and possibly more efficient. However, do they have more functionality? The Reserve Bank of India believes that AAs have a role to play in making financial products and services more accessible. Let’s test that hypothesis, shall we?

One of the primary reasons why financial services are not fully utilised is a mutual trust deficit among users and FSPs. This trust deficit tends to manifest itself in different ways for these two types of actors in the ecosystem. FSPs believe that there is rampant non-payment, negligence in provision of information and fraud by users. Such users on the other hand often complain of their personal data being sold for profits and misused as a result of unsafe and unauthorised data transfers.

A useful example of this is lending. Jigneshbhai felt the need to track his borrowers because he could not ascertain his borrowers’ repayment discipline. The tracking and the general spying was therefore an assurance of his returns. With his institutional counterparts, such assurances are derived from the underlying physical or financial collateral provided by the borrower which is re-assessed at regular intervals. If a borrower is unable to provide adequate assets for collateralisation, lenders cannot trust users to hold up their end of the contract and cannot justify sanctioning loans to them due to the inadequacy of proof of their ability and willingness to repay.

Similarly on part of the users, it is evident that most financial activities require a plethora of documents and a number of signatures, all of which keep many gainfully employed during ‘banking hours’ across India. As Pankaj Kapur’s iconic performance in ‘Office Office’ remains the source of much good humour among many, the app based world of finance has credit card frauds and scam calls from sold personal data (refer the Netflix series ‘Jamtara’ for more sordid details). Suffice to say, in the absence of assurance of secure movement of data, most users find it difficult to trust and experiment with financial products and services.

AAs play an important role in addressing these concerns.

First, they permit users to control who has access to their data, track and log movement of data and reduce the potential risk of leakage in transit.

Second, the single window format allows movement in a hassle free manner and reduces the need for physical transfers and post facto attestations. AAs create an operating procedure for consent which becomes the default industry standard that cuts through the heavy handed fine print buried in privacy policies.

Finally, with security of this data as a given, AAs can allow lenders (or other FSPs for that matter) to rely on a wider selection of data points that indicates the trustworthiness of a business and their existing track record. This tightens the risk associated with deploying financial products, allows FSPs to tailor payments and requirements to the user and build more customised products which are less likely to go bust. It gives FSPs room to allow businesses with non-traditional models or credit backgrounds to participate in the financial ecosystem.

All in all, by transferring consent-based data from FIP to FIU through AAs, FSPs have a chance to provide flow-based credit, personal financial management tools, robo-advisory services and many more innovative financial products and services to a wider cross-section of people. As financial institutions get smooth consent-based access to financial data, they can offer better suited products to the user and improve access to such tools.

Are there any drawbacks then?#

While AAs are no doubt an important tool in the arsenal for achieving universal access to financial services, this access (or the lack thereof) is a spectrum. At the two ends of the spectrum are users that access all available products in the market to achieve the best financial outcomes for themselves and users that fall outside of the financial ecosystem completely and are in fact potential customers.

AAs may be useful in chipping away at the trust deficit one consensual data transfer at a time but in reality a large part of the unbanked and unserved are also data poor. In such cases, the benefits of the AAs will be available after the initial hurdles of data gathering have been crossed.

To wrap it up, the value addition that the AA framework brings to the financial ecosystem is tremendous and once implemented in full it is all set to bring about the security, transparency and agility that the financial services sector needs.

If you're looking to use Account Aggregator in your app, sign up to our sandbox right away! You can try, test and implement AA APIs within minutes.