The similarities and differences between UPI and Account Aggregator

Pete

Head of Growth

17 Mar 2023 — PRODUCT

ACCOUNT AGGREGATOR

Do you maintain excel sheets to track your monthly spending? Have you downloaded and shared your bank statements while applying for a loan?

Account Aggregators are going to eliminate these pesky tasks. For good. Sign up for Setu Account Aggregator here.

Account Aggregator (AA) is a framework that was introduced by the RBI to make data sharing across financial institutions more transparent and easy. It is the next big thing in fintech. As tempted as we are to call it the ‘UPI moment for data’, we’re going to hold off.

It’s time someone stepped in and cleared the air.

Well, during most of our sales conversations and group discussions, we realised that the UPI analogy is being overused in the Account Aggregator context. Sure, there are similarities between UPI and AA. But there are also some stark differences. In this article, we will be going deep into some of the similarities and differences between UPI and AA. And hopefully, put the analogy to bed.

Both UPI and Account Aggregator are DPIs or digital public infrastructures. As you might have read countless times, DPIs are the main reason why our country is at the forefront of fintech innovation.

How?

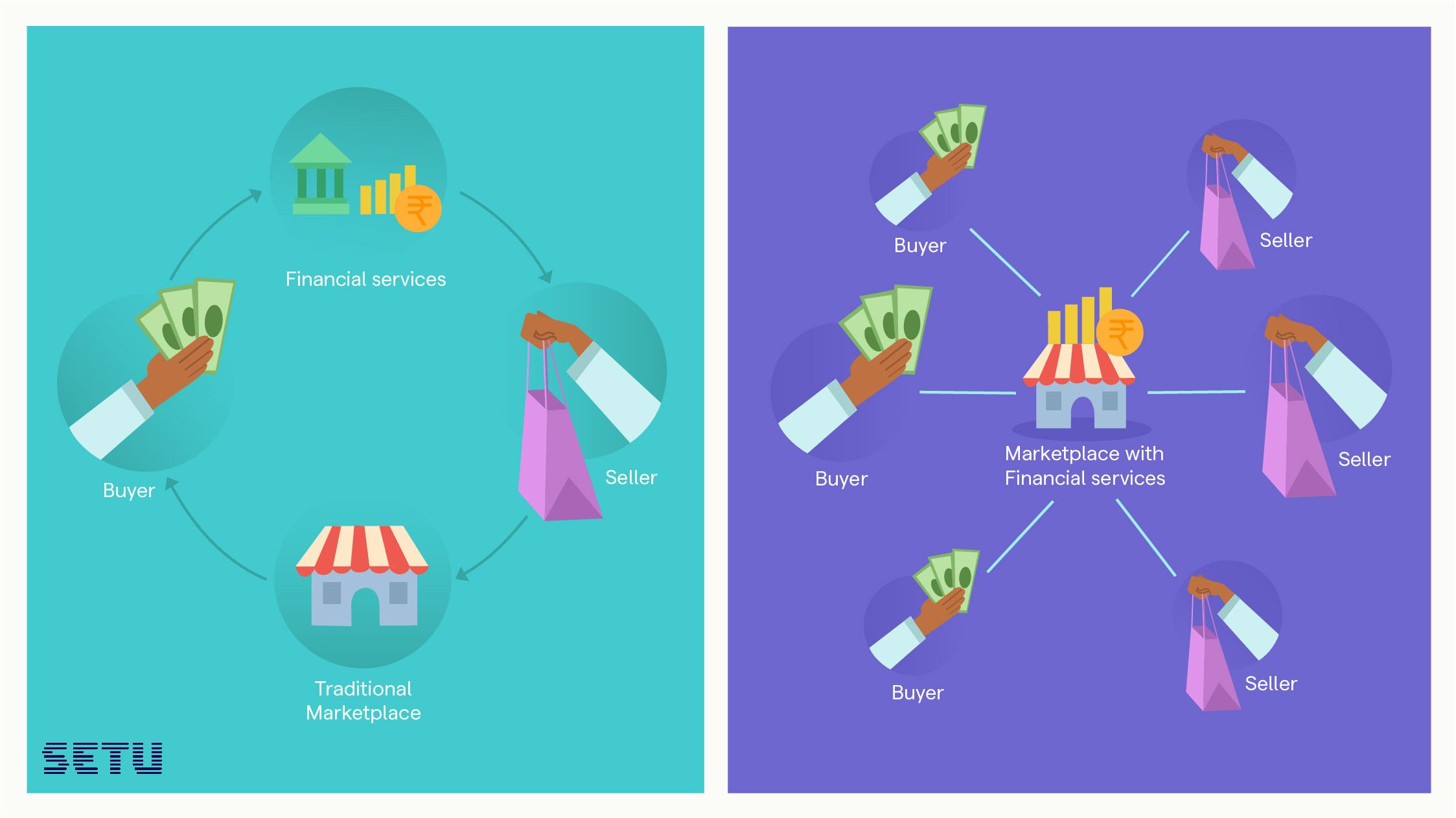

Unlike the West, whose finance sector growth relied heavily on private companies and banks expanding, India has taken a different approach. India built digital infrastructure for various aspects like identity, payments, taxes, and data on a common, public platform. Then, India opened the doors for private players to build applications on top of these public digital infrastructures leaving room for markets to be created and innovation to thrive! For example—Google built the popular payment app, GooglePay on the UPI infrastructure. This is a great example of how DPIs can fuel growth.

A right balance between regulation and innovation.

Now, this is made possible because all DPIs are interoperable, standardized in their specifications (AKA “Specs”), and have open APIs. This means that companies can use these open APIs and build unique use cases for their customers. For example— a B2C neo-bank could go live on Account Aggregator and offer real-time spending analysis for their users. A lending institution can eliminate the need to ask borrowers to upload a 10-page bank account statement and switch to a completely digital way to fetch bank statements.

This is similar to how UPI is designed. GooglePay is being used by several of us to transfer funds to our friends and Setu’s UPI stack is used by several businesses to collect payments from their users. All these use cases are possible because of the open APIs that UPI and AA are built on.

This is one of the key differences between UPI and AA. UPI is an instant real-time payment system that is used to transfer funds between two bank accounts. An HDFC bank user can send money to an IDFC bank user instantly if they both use apps built on UPI. As you can see, the UPI Infrastructure is connected to only banks, because it’s focused on moving money i.e., payments.

Account Aggregators, on the other hand, are linked to all types of financial institutions like NBFCs, Insurers, depositories, banks, and several others. Since the unit of transfer is data and it is run in collaboration with multiple regulators, it has much wider scope. Using an Account Aggregator, a fintech app can request data from their users on all their financial accounts—like LIC for Insurance data, HDFC for transaction data, and NSDL for Investment data— and offer personalised services to them.

Hopefully, pretty soon we’ll stop getting random calls asking if we’re looking for a housing loan in the middle of a vacation. What even, right?

The involvement and buy-in of multiple large financial institutions in the AA ecosystem is a true indicator that AAs will soon change how financial services are being offered and consumed in our country.

This one is a little tricky to answer.

Let’s break down the role of NPCI in the UPI ecosystem.

From a technical standpoint, NPCI acts as the trusted ‘switch’ or central processor and orchestrator between banks and payment apps and makes sure that money flows are routed to the correct and verified destinations. Payment apps and banks interact just with NPCI and can be assured by NPCI that they are really interacting with who they intend to. NPCI also plays the role of an evangelist—as they push the boundaries with newer features, variations, and partnerships. Their audacious mission of facilitating 1 billion UPI transactions per day is a testament to their evangelism.

Finally, there is the question of their organizational structure and type. NPCI is an NUE or “New Umbrella Entity” that is designed and authorised by the RBI to manage payment systems in India. They are a non-profit entity that is given authority by the RBI to create guidelines for the payment systems they govern.

In the AA world, these responsibilities are bifurcated. For starters, each account aggregator acts as the trusted “data switch” between the platform requesting data and the entity from which the data is being fetched. Since all Account Aggregators are RBI-regulated entities, each of them has to adhere to strict policies to ensure fair and responsible behavior.

The role of the evangelist is played by Sahamati. Sahamati (DigiSahamati Foundation), is an SRO or Self Regulatory Organization, or a member-driven industry alliance formed to promote and strengthen the Account Aggregator ecosystem. They are a collective of people and organisations from different backgrounds like finance, law, and technology to set and achieve audacious goals for the Account Aggregator network.

These are some of the common similarities and differences between UPI and AA. Stay tuned for Part 2.