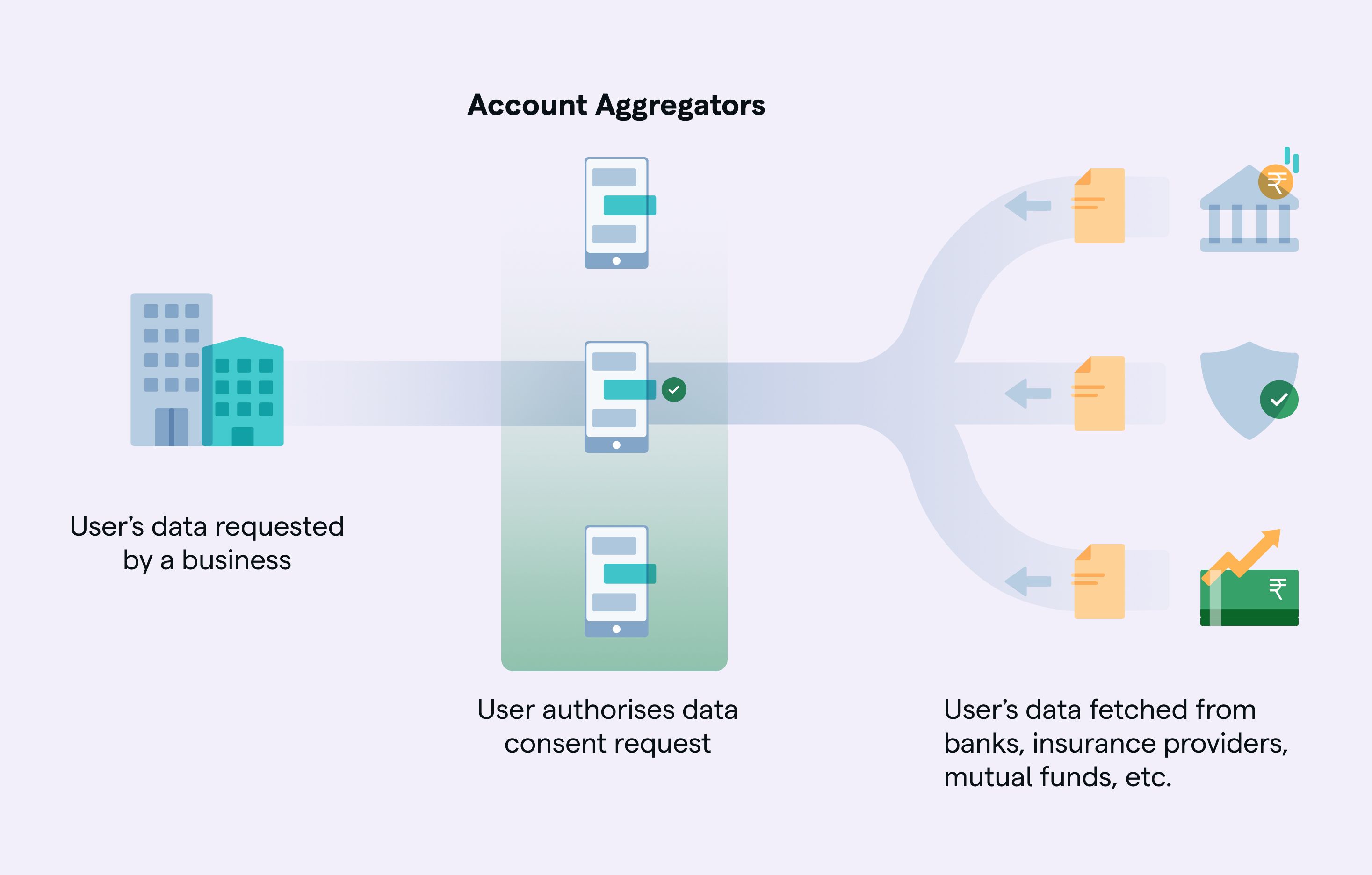

What on earth is an Account Aggregator gateway?

Pete

Head of Growth

31 Oct 2023 — PRODUCT

ACCOUNT AGGREGATOR

Quick recap: The Account Aggregator ecosystem has grown tremendously over the past two years. Today, the total number of cumulative accounts linked stands at 22 million (September 2023). While this is still fairly low compared to other DPIs (Digital Public Infrastructures) like UPI and BBPS, the stage is set for massive adoption.

While we’re probably closer to the Account Aggregator inflection point than ever before, we’ve noticed some common patterns. This is our attempt to explain some of these patterns and hopefully, stop some of you from making similar mistakes.

In sales discussions, I often rely on the payment gateway example as my go-to analogy.

Let me explain.

Every large online business in our country uses multiple payment gateways. A company the size of Flipkart would probably be using at least ten.

What I mean to say is that it is extremely risky for any online business to depend on only one payment gateway. Even in this day and age of fintech advancements, the number of payment failures, bank downtimes, and other scenarios is high. So, depending on one payment gateway is not only risky but it’s just not smart. A 5 min downtime can cause several customer drop-offs and it’s damn near impossible to get those customers back. Especially if they are new ones.

To prevent these scenarios, online businesses work with multiple payment gateways. If they notice any stability issues in one, they route their users to another PG. Long story short, it is important to not put all your eggs in one basket.

Similarly, companies must not partner and rely just on a single Account Aggregator. A small downtime can cause a broken experience that cannot be salvaged. Imagine a borrower left stranded at the last leg of a digital onboarding journey because his data could not be fetched. Or a user logging in to his PFM app to realise that her transactions for the past 24 hours could not be fetched and thus not categorized.

Instead, companies should partner with multiple Account Aggregators to handle traffic or work with an Account Aggregator gateway. I’ll explain what an AA gateway is towards the end of this piece.

Now, partnering with multiple AAs has a lot of long-term benefits. But there is also an important short-term benefit to this.

FIP Coverage.

Today, FIP coverage is not standard across all Account Aggregators. Meaning, not every FIP is live with every Account Aggregator.

There are about 10 Account Aggregators and 117 FIPs in the ecosystem today. Each Account Aggregator has to directly integrate with each FIP. Now, there are only 31 FIPs that are live with at least 5 AAs. Only about 9 of them have already integrated with at least 8 or more AAs. This means that a large chunk of FIPs work with only a few AAs. 87 FIPs work with less than 4 AAs. 56 of them are live on only 1 AA.

46% of all the active FIPs are live only on 1 AA.

Check FIP to AA mapping here.

Pretty shocking isn’t it?

Well, to be fair to us we did mention that this is short-term.

Yes, FIP coverage isn’t standard across all AAs today. But this will improve over the next few years. Plus, there are newer AAs coming up so this will take its own sweet time to improve.

With this groundwork laid out, discerning the right partner becomes critical.

See, we understand that the AA ecosystem is pretty complex and dynamic. New FIPs are being onboarded, new AAs are coming up, newer versions of the API schema are getting released, and use cases keep broadening.

This is why **partnering with a technical service provider or TSP will be your most important decision. **

Simply put, a TSP absorbs a large chunk of the regulatory and operational complexities involved in using the Account Aggregator infrastructure. TSPs usually have their ear close to the ground, help FIUs understand which FIPs are performing well, and make UI/UX changes to drive higher and higher conversions.

Crucially, a TSP like Setu also partners with multiple Account Aggregators and provides, what we call, an Account Aggregator gateway.

We manage the back-end orchestration of a data fetch through multiple Account Aggregators and FIPs based on factors like success rates, coverage, and performance.

TSPs also have another unique advantage over Account Aggregators. Account Aggregators are mandated to be in the business of Account Aggregation and nothing else. This restricts them from adding any value-added services on top. An AA fetches raw data from a FIP and delivers it to the FIU. That’s it.

TSPs, on the other hand, do not have this restriction. They can analyse the raw data that they receive from FIPs and deliver meaningful insights for various use cases. A TSP can offer analysed bank statements to lenders for quick underwriting. It can provide an exhaustive transaction categorisation engine for any fintech app.

Endless insights delivered in custom formats.